Hermann Hauser in a recent article on Project Syndicate, entitled “The Struggle for Technology Sovereignty in Europe” argues for “the UK and EU to jointly establish a €100 billion ($120 billion) Technology Sovereignty Fund to counter the $100 billion that the US is spending on its technology sovereignty and the even larger amounts China is mobilizing”. I argue here, that we should be thinking that 27+1 countries could create much larger funds in a world where single individuals like Masayoshi Son can create funds of that order.

Hermann Hauser became an entrepreneur right after finishing his PhD in the Cavendish Lab (Cambridge University, UK) around 1978 – on the same lab bench in the Cavendish as myself – and is arguably Europe’s first and most important technology venture investor. Hermann Hauser can be seen as the initiator of Europe’s VC industry. Hermann Hauser is also one of the co-founders of ARM and many other high-tech companies. For a discussion with Hermann see:

The thought of a €100 billion Technology Sovereignty Fund is of course a fantastic plan. As a starting point, thats of course a great idea, however in my opinion, much much more is needed. My thought would be that for European Technology Sovereignty, five or ten, or even more funds of that €100 billion size will be needed. In my opinion, better not only by governments, but by private individuals like European versions of Masayoshi Son.

Three thoughts, which I will illustrate below

a €100 billion fund for 27+1 countries is a lot smaller than the US$ 391 billion the single man Masayoshi Son is estimated to control (Vision funds plus three companies)

a €100 billion fund for 27+1 countries is much smaller than the sovereign funds of very much smaller countries:

Singapore (5.7 million people), sovereign funds: US$ 715 billion

Norway (5.3 million people), sovereign funds: US$ 1327 billion

My third point is that the assets in question (ARM) in Hermann Hauser’s Project Syndicate article would already use a large part of the proposed €100 billion fund.

To put a €100 billion fund for 27 EU Countries + UK into context:

Just one single man (Masayoshi Son, from a Korean immigrant family to Japan) controls at least two funds + and to some extent several companies, worth in total on the order of US$ 391 billion as follows:

the current “fair value” of the first + second Vision Funds is reported as US$ 154 Billion.

In addition, Masayoshi Son also controls (to some extent) the listed companies, which he often uses as acquisition and finance vehicles:

SoftBank Group Corp [TSE: 9984]: market cap = US$ 130 billion

SoftBank Corp [TSE: 9434]: market cap = US$ 67 billion

Z Holdings Corp [TSE:4689]: market cap = US$ 40 billion (includes Yahoo Japan Corp + LINE)

That is just one single man, who created all this from zero, not 27+1 countries.

Or as another comparison, Singapore has built at least two sovereign funds in total estimated to be worth US$ 715 billion. Singapore is one single relatively small country compared to 27+1 European countries (population of Singapore is about 5 million, about the same as Norway, and about the same as the Berlin region)

Singapore Sovereign Wealth Fund GIC estimated value US$ 488 billion

Temasec Holdings US$ 227 billion

Norway’s sovereign funds (population about 5 million):

Sovereign Pension Fund – Foreign US$ 1300 billion assets

Sovereign Pension Fund – Norway US$ 27 billion assets

My third point is that a single €100 billion fund is of comparable size of developed assets in question. eg. ARM’s current value would be a substantial part of a potential €100 billion fund. This means that after acquiring two or three companies of the value of ARM this fund would already be exhausted.

As another example, the strategic German mRNA company BioNTech (which among other therapies developed the BioNTech Covid Vaccine in cooperation with Pfizer) has a current market cap of US$ 51 billion. If a situation would arise that such a Sovereign fund would acquire a company such as BioNTech, that would again use up a large fraction – if not almost all of this fund. In my opinion, although of course a €100 billion fund investing in European technology companies in addition to existing substantial VC and investment funds would be great, this is not huge – even relatively small – compared both to the value of many assets in question, and also to the funds some private individuals (eg Masayoshi Son) or 5 million people countries (like Singapore or Norway) manage to build.

So I think many more than a single €100 billion fund would be needed for Technology Sovereignty – I hope circumstances will develop where even more can be invested in European ventures than today. Hermann Hauser’s proposal is certainly a great step in the right direction- many more such steps would be great!

Hermann Hauser is co-founder of Acorn Computers, Advanced RISC Machines (ARM) and arguably the most distinguished leader of Cambridge’s Venture Ecosystem.

Recording of the video discussion:

On Thursday 17 September 2020 at 6pm we will meet in central Tokyo.

Hermann Hauser- Europe’s venture capital pioneer, and co-founder of ARM and many other companies and investor in unicorns – has very generously agreed to hold a video discussion on Thursday 17 September 2020.

Hermann did his PhD at the Cavendish Laboratory (on the same lab bench as Gerhard Fasol), then became co-founder of Acorn Computers, and several other laboratories and companies, including Advanced RISC Machines (ARM). Hermann is arguably one of the most important leaders of the Cambridge venture ecosystem.

Bill Emmott is an independent writer and consultant on international affairs, board director, and from 1993 until 2006 was editor of The Economist. http://www.billemmott.com

Gerhard Fasol is physicist, board director, entrepreneur, M&A advisor in Tokyo. https://fasol.com/

Japan’s future: A conversation

Bill Emmott:

I came first to Japan in 1983 as Economist Tokyo Bureau Chief, staying until 1986. Then in 1988 I came back on sabbatical leave and wrote “The sun also sets: why Japan will not be number one”, which against my expectation when it was published in 1989 found big resonance in Japan. The stock market was plunging, and mine was the most immediately available explanation. Ever since, journalists have constantly asked me what the sun is doing now! It also meant that even when I became editor in chief of The Economist in 1993 I spent much more time focused on Japan than I had expected, visiting as often as I could to keep track of the post-bubble developments, and wrote a book that appeared only in Japanese translation called “Kanrio no Taizai”, or the bureaucrats’ deadly sins. But later, with Prime Minister Koizumi consolidating reforms, and the banking system at last getting cleared up, I sent myself back in 2005 to research and wrote a much more optimistic special supplement for The Economist which became a book, “The sun also rises”.

Throughout the 35 years since I first came to Japan, I have both been fascinated and struck by the fact that although this is in so many ways an inward-looking self-contained nation, foreign observers are listened to and even have a chance of having a positive impact.

One element that had featured consistently in my writings ever since the 1980s had been observations and expectations for a growing role for women in employment and power. This seemed logical given that, at least before the bubble burst, Japan was heading for a labour shortage, but also the Equal Employment Law of 1986 had led to more females being recruited by major organisations. Japan’s excellent education surely meant that the underused half (= women) of the adult population would soon be used more productively.

Of course, this has developed a lot more slowly than I expected or hoped, partly for cultural reasons but also because Japan has not in fact had a labour shortage, until now.

I wanted to meet you, Gerhard tonight because we both are fascinated by the role Japanese women have in making Japan such a fascinating country, and how the many really strong Japanese women could have key roles in bringing growth and dynamic change back to Japan.

Could Japanese women have bigger roles for the development of Japan?

What is holding women back in Japan?

Who are the role models?

I am making interviews with high-achieving Japanese women to try to find answers, and plan to compile them into a book later this year. What would you say, Gerhard? And anyway, how did you end up here?

Gerhard Fasol:

My path to Japan is quite different than yours, Bill. I came to Japan first in 1984 as Fellow of Trinity College Cambridge, and scientist at the Max-Planck-Institute in Stuttgart, part of a project to build a research cooperation with NTT’s R&D labs. I saw that Japan was very important in technology and weakly linked to the outside – and still is today, I think. So in 1984 I decided to make Japan my second professional focus in addition to physics and electronics. Like you – the deeper I get into Japan, the more I learn about Japan, the greater my fascination, and my motivation to contribute.

Now I am working on many different projects, working on international technology M&A projects, and I am also one of a microscopic number of foreigners on the Board of Directors of a stock market listed Japanese corporation – reforming Japanese corporate governance hands-on.

Could Japanese women have bigger roles for the development of Japan?

Gerhard Fasol:

I think that the equal participation of women in leadership is directly linked to the population issue, ie the number of children born.

while in Sweden 44% of Members of Parliament are women,

37% in Germany and

26% in France –

the world average is 23% women in Parliaments.

In Japan the ratio of women in Parliament has increased from 1% in 1990 to 10% in 2016, so there is progress. If we extrapolate, and if the trend continues, then it might take another 30 years or so until Japan reaches world average in terms of women bringing women’s views into Parliament, and taking part in making the laws. And it might take Japan 100 years to reach Scandinavian standards of women’s participation in making the laws of the land – unless there is some acceleration in Japan.

Japan’s most powerful Ministry, the Ministry of Finance, did not hire any women into career positions for a period of about 10 years!

At the 2015 New Year event of Kyoto Bank, Keidanren Chairman Mr Sadayuki Sakakibara showed that Japan’s spending on aged people is dramatically higher than spending on children, and that this ratio is increasing with time, Japan spends more and more on aged people and less and less on children. There are two ways to look at this situation:

one way is to say: we have an aging society, therefore its only natural to spend more on

the aged, and less for children

the opposite way to look at the same situation is to say: we are spending less and less for children, no wonder we have fewer and fewer children. If we did more for young people, maybe people will have more children….

Actually most Japanese women I talk to want 2-3 children, but many cannot for financial reasons.

By nature, women give birth to children, not men, so more women in decision making positions including Government and Parliament will bring children’s issues into decision making.

As an example, child birth costs in Japan are not covered by health insurance, while they are everywhere in Europe. There are many other open and hidden costs of having children in Japan compared to Europe.

The most important factor are mindsets. The key to give more power to women in Japan is to change mindsets, to change the way of thinking.

As an example, the Prefecture of Kanagawa in 2015 created the “woman act” committee, under the slogan “women, step by step, take more responsibility”, however this committee both in 2015 and also in 2016 consisted of 11 men – not one single woman leader – here with original photographs archived on the wayback-machine / internet archive

Why not create a committee of 11 women leaders to lead efforts on gender equality in Kanagawa Prefecture? Why not promote women to leadership positions in Kanagawa Prefecture?

Another factor holding women back are the very long working hours common in Japan. As an example, at a recent EU-Japan gender equality conference, the Danish polician Astrid Krag, who was Minister for Health and Prevention at the age of 29 – 32 years, and who has two children, explaned that in the Parliament of Denmark the decision was taken not to take any vote after 4pm, so that Members of Parliament can be back home by 5pm, collect children from daycare centers in time etc. So in the Parliament of Denmark it is guaranteed that Members of Parliament can leave at 4pm. In today’s Japan such action is unthinkable, age 29 – with young children – would be unbelievably young for a Government Minister in Japan. https://en.wikipedia.org/wiki/Astrid_Krag

Late-night or overnight sessions at work, including Parliament, makes life incredibly difficult in Japan for parents with young children, doubtlessly contributing to the small number of women in top positions in Japan.

Who are the role models?

Gerhard Fasol:

Despite these difficulties, there is a substantial number of very strong women in Japan, who have worked their way up into leadership positions.

Examples are the Mayor of Yokohama, Ms Fumiko Hayashi, who succeeded in a very distinguished business career, and the Governor of Tokyo, Ms Yuriko Koike, who won the election on her own as an independent candidate, because she did not receive the backing of her party.

Bill Emmott:

That is great, as I have now interviewed Koike-san and plan to interview Hayashi-san during my next visit. Personally, as well as admiring women who have made it to the top in the tough political world I also admire and am interested in women succeeding as entrepreneurs and as executives in entrepreneurial companies. By starting and building their own companies, women can really create new realities, showing that new organisational cultures are possible in a Japanese context. Do you agree?

Kyushu University has one single full Professor of Medicine Professor Kiyoko Kato, she explains the situation of women in Japanese Obstetrics and Gynecology here https://www.boltzmann.com/2016/05/kiyoko-kato/ while Professor Kyoko Nomura has built a center to support women medical doctors and women medical researchers at Teikyo University. She spoke about the situation facing women in medicine in Japan here: https://www.boltzmann.com/2016/02/kyoko-nomura-2/

Towards the future

Gerhard Fasol:

The tantalizing issue is that the key is to change mindsets, and thats at the same time superficially easy, but at the same time incredibly hard. Thus outstanding strong Japanese women – and there are many of them – have a choice either to work their way up to the top in Japan, start their own company in Japan, or on the other hand to move to Europe, elsewhere in Asia, or to the USA – I know several strong Japanese women, including several Japanese medical doctors, who have moved to Europe or USA. They might of course come back to Japan at a later stage bringing global views and experiences to leadership positions in Japan in the future. I am very optimistic for the future of Japan – sometimes I wish things were moving faster.

Bill Emmott:

I agree entirely. I see Japanese women as both victims of the slow speed of change and as solutions to it. They really could make the Japan of 2030 look quite different, in all sorts of ways. It will be fascinating to watch.

Bill Emmott and Gerhard Fasol met at the restaurant MusMus in Tokyo

left to right: Gerhard Fasol, Ms Atsuko Konta (Manager of the restaurant MusMus), Bill Emmott at the restaurant MusMus in Tokyo.

Copyright (c) 2017 by Bill Emmott and Gerhard Fasol. All Rights Reserved.

Japan’s globalization puzzle: intriguing questions by one of my great European friends, a great European banking sector leader

How do you explain Japan’s lack of internationalization with so many big Japanese holdings managing successfully businesses abroad (e.g. Toyota, Toshiba, Mitsubishi, etc.)

Japan’s globalization paradox – a closer look

Its not so simple: Japan is a huge country, third globally, and there are 3500 Japanese companies listed on the Stock Exchanges – they are all different. Some Japanese companies are very excellent and successful and global leaders or even No. 1 in their fields – e.g. you mention Toyota and there are many more.

There are two main factors limiting Japan’s growth

decreasing and aging population. few babies and no immigration.

structural reasons (slow growth by traditional established corporations, and too few new high-growth industries), corporate governance issues, addressed by Prime-Minister Abe’s “third arrow”, however most people agree that Prime Minister Abe’s “third arrow” reforms have been more words than action. Maybe the most or only successful “third arrow” reform are Japan’s corporate governance reforms

You mention Toshiba – Toshiba is a famous global brand in many sectors, and Toshiba has developed many important technologies in many areas from medical technology (Toshiba’s medical sector has been sold to Canon as a result of Toshiba’s accounting scandal), semiconductors (especially flash memory), but Toshiba’s profits/income averaged over 20 years is close to zero, ant Toshiba did not grow for 20 years, and went through a series of accounting scandals etc. Now as a consequence of these scandals, Toshiba has to sell off several important growth divisions, e.g. their very valuable medical technology sector to Canon. Read comments on Toshiba here: http://www.eurotechnology.com/2015/07/21/toshiba-income-restatement/

or read in Wall Street Journal about Toshiba here 2 days ago http://www.wsj.com/articles/toshibas-turnaround-needs-more-work-1471007429

Toshiba’s accounting issues are the result of a combination of mainly two factors:

20 years no growth and essentially no profits, compounded by financial problems in the nuclear industry segment as a consequence of the Fukushima Dai-Ichi nuclear disaster (Toshiba had acquired the nuclear manufacturer Westinghouse, and thus is a major nuclear industry manufacturer and contractor)

corporate governance

Companies such as Toshiba, benefit from their globally famous brand, therefore I am quite optimistic that Toshiba and other Japanese companies in similar situations can recover, if the correct management decisions are taken, and if corporate governance is improved – and this is exactly the reason why the current Japanese government sees corporate governance reforms in Japan as a major priority.

There is no doubt in my mind, that if corporate governance, management and other factors are improved, companies like Toshiba can be transformed into iconic companies, but these will be different companies than today.

As an example, both SONY and HITACHI are quite successful in their revival efforts.

Mitsubishi – there is no Mitsubishi Holding Company, but 1000s of companies with Mitsubishi in their name…

As another example you mention is Mitsubishi. There is no single company with the name “Mitsubishi” in Japan. There are 1000s of companies with Mitsubishi in their name, and most are loosely grouped into the Mitsubishi Group – which is not a legal entity, and at their core is Mitsubishi Trading Company, and Tokyo Mitsubishi UFJ Bank etc. In some cases there are cross-shareholdings within the Mitsubishi Group, but these have been reduced much over the recent years. There is no “Mitsubishi Holding Company”. Most companies with Mitsubishi in their name are independent companies, many independently on the stock exchange.

Together the Mitsubishi ‘Group’ is a big part of Japan’s economy – maybe 10-15%, but the ‘Mitsubishi Group’ is not a corporate group in the Western sense. Some of these companies are very successful and very strong – some are very good, but some have difficulties – which can also be overcome. An example is Mitsubishi Motors, an automobile maker, which was acquired around 2001 and then divested again in 2004-2005 by Daimler (then Daimler-Chrysler), and is currently being reformed by Nissan under the guidance of Nissan/Renault CEO Carlos Ghosn.

(Masamoto Yashiro is my great friend and a legend in Japan’s banking and energy industry. He built Shinsei Bank from the ashes of the bankrupt Long Term Credit Bank of Japan, and served in leadership positions (Chairman, CEO, Board Member) in Esso, Exxon, Citibank, Shinsei Bank, and the China Construction Bank)

The photograph shows the Gobelsburg Castle in Austria, you can see the location here on Google maps. A castle of this name is mentioned in 1178, and wine is grown in the region for about the last 1000 years.

www.fasol.com

Thoughts and analysis for 2015

Abenomics?!

The trick of course is the third arrow, the reforms. Read what Professor Takeo Hoshi has to say about Abenomics, Japanese economist, who has worked his way up US Universities, and has now reached the position of Professor of Economics at Stanford University. By the way, here is my talk at Stanford University – some years ago, but much of it still applies today.

Japanese people’s views on nuclear power are polarized, and its unclear and unpredictable when nuclear power stations will be switched on again in Japan. Read what the Governor of Niigata Prefecture has to say, who hosts the world’s largest nuclear power plant with 7 reactors and 8 GigaWatt capacity.

According to the Japanese Energy Fundamental Law, the Government has to publish an official Energy Basic Plan at regular intervals. You can read the 4th Energy Basic Plan published on April 11, 2014, and listen to a commentary on it for The Economist here on YouTube. The 4th Energy Basic Plan starts with the assumption that Japan is poor in natural energy resources, which of course is only true if we restrict “natural energy resources” to fossil resources. Japan is actually potentially very very rich in renewable energy sources, as the scenario plans developed by Japan’s Industry and Economy Ministry (METI) and Japan’s Environmental Ministry show.

Foreign companies in Japan, and Japanese companies overseas face a dilemma: expensive expatriates with limited local know-how, or local management? Japanese companies seem to have finally reached the conclusion that Japanese managers eg sent to Germany are in most cases not the best choice to lead a German-based multinational company – here are some great recent examples:

Docomo acquires a majority stake in net mobile AG, however net mobile AG remains a publicly listed company. Read details here.

NTT DATA acquires SAP solution provider itelligence AG, however itelligence AG remains an independently managed company under the founder’s management, and grows aggressively via acquisitions all over the globe. Read details here.

NTT Communications acquires a majority of Integralis, Integralis is renamed NTT Com Security AG, however NTT Com Security AG remains traded on the m:access market of the Munich Stock Exchange. Read details here.

Carlos Ghosn is very well aware of such multi-cultural management issues and how to solve them, however too many EU companies in Japan are not. If they were, EU investments in Japan could be at least 50% higher – as you can read here.

Lunch today (22 Nov 2013) with the Trade Minister of Sweden, Dr. Ewa Björling, chaired by the Ambassador of Sweden. Was asked to brief Minister Björling and a delegation of Swedish CEOs about Japan’s energy sector. Gave Minister Björling a 20 minutes presentation followed by discussion.

Dr. Ewa Björling is extremely impressive, she is dentist, teaches virology at Karolinska Institutet, is Deputee of Rikstaget (the Parliament of Sweden), and Trade Minister of Sweden. According to Dr. Ewa Björling’s website, she plans to double Sweden’s exports within five years.

Professor Takeo Hoshi, Professor of Economics at Stanford, about Abenomics success probability

Why did Japan stop growing after completing the catch-up with advanced countries?

Takeo Hoshi, Professor at Stanford University, who devotes his life to work on Japan’s economy at US Universities, gave a talk at the Swedish Embassy organized by the Stockholm School of Economics on Monday, October 21, 2013 entitled:

Will Abenomics restore Japan’s growth?

Outline:

What is Abenomics?

Will Abenomics restore growth?

Why did Japan stop growing?

Will Abenomics succeed in regenerating growth?

Professor Takeo Hoshi

Summary – Abenomics success probability:

Professor Hoshi explained that Abenomics is essentially nothing new, its the classical response for a Government to take a country out of recession. However, monetary policy cannot restore growth – in order to restore growth structural reform is needed.

Why did Japan stop growing? Until 1990-1995, Japan was in catch-up mode, catching up with the more technologically and economically advanced Western countries, like European countries and US. Catching up was relatively straightforward, because Japan’s Government could look which industries were most successful and most important in US and Europe, e.g. car industry and electronics industry, and steel making, and then implemented these industries in Japan. However, as soon as Japan had reached the same stage of development as Western countries, Japan’s economic growth stopped, because different methods were necessary, and they seem to be lacking in Japan. So Japan stopped growing around 1990-1995, and has not grown since.

Growth strategy is the “third arrow” of Prime Minister Abe’s Abenomics. Professor Hoshi explains that a growth strategy is nothing new, but every Japanese Government of recent years had a growth strategy, but nothing happened because the implementation did not happen – implementation is the key. Abenomics’ “third arrow” lists more than 100 growth areas, however, Professor Hoshi sees a lack of priorities, too much Government directionalism, and a lack of strong Key Performance Indicators (PKI’s).

When asked during Q&A how high Professor Hoshi estimates the chances for the success of Abenomics, Professor Hoshi said that he estimates that the probability for success of Abenomics is about 12%, and the probability of failure is about 88%. The most likely scenario according to Professor Hoshi is that something similar will happen as under Prime Minister Koizumi, about 1% economic growth

What is Abenomics:

Three arrows:

Expansionary monetary policy

Flexible fiscal policy

Growth strategy

Prime-Minister Abe replaced Shirakawa by Kuroda as Governor of the Bank of Japan, who introduced quantitative and qualitative easing, and an inflation target of 2% within 2 years in order to overcome “deflation” (which in Japan can have two distinct meanings, see below).

Fiscal Stimulus:

Fiscal stimulus was provided by supplementary budgets, financed by new Government bond issues.

Fiscal consolidation plan:

The medium term fiscal consolidation plan aims to:

reduce the budget deficit to 3.3% of GDP by FY2015, to half the level of FY2010, and

to eliminate the budget deficit by FY2020.

If the 2013-2022 economic growth rate is 3.4% per year, 1. (reduction of budget deficit 10 3.3% by FY2015) will be achieved, but 2. (elimination of budget deficit by FY202) will not be achieved.

If the 2013-2022 growth rate is 1.3% per year, neither 1. nor 2. will be achieved.

Growth strategy

The “Japan revitalization strategy” (JAPAN IS BACK) was approved by the cabinet on June 14, 2013, and provides:

3% average nominal economic growth

2% average annual real growth

YEN 1.5 million increase in nominal national income per person

Three action plans:

Industry revitalization plan

Strategic market creation plan

Strategy of global outreach

Overcoming “deflation”?

Abenomics aims to overcome “deflation”. Deflation really has two meanings:

Falling prices, because of low demand for goods and services

Economic stagnation in combination with falling prices

In Japanese policy discussions, usually “deflation” has the second meaning – thus its important to restore growth in order to eliminate “deflation”.

Is Abenomics new?

Not really. It is the standard policy to get out of recession and to restore growth. Its a combination of demand policy and a supply side policy for growth. What is new in Japan is that until Abenomics, the Bank of Japan did not expand aggressively, and it could be new in Europe, where fiscal austerity is a problem.

Why did Japan stop growing?

Mainly because Japan’s catch-up phase with Western countries has been a success, and Japan reached the same level of technology and economic development as Western countries around 1990-1995. The catch-up was straightforward by imitating in combination with lower wages. As soon as Japan reached the same level of development as Western countries, Japan’s economic growth stopped.

However, US and UK and other Western countries continue high growth of GDP even at high levels of economic development, while Japan does not.

Why does Japan grow much less than US, EU and other Western countries?

Because Japan’s population is aging more rapidly than Western countries, because of lower fertility rates and lack of immigration

Because the export led growth has reached its limits, and internal growth would be necessary

Because Japan’s Government make policy mistakes:

Japan’s Government protects zombie companies, that hurt allocation of capital and productivity

Regulatory policies impaired productivity growth

Macroeconomic policy mistakes

Will Abenomics restore Japan’s economic growth?

Fiscal policy cannot restore economic growth, only structural reform can – thus Abenomics’ “third arrow” is the important one.

Japan revitalization strategy – too many areas, too little focus, fuzzy Key Performance Indicators (KPIs)

Prime Minister Abe’s revitalization strategy has three action plans:

Industry revitalization plan

Strategic market creation plan

Strategy of global outreach

Regulatory reform aims to reduce the costs of doing business, to stop protecting zombies, and “special zone” policies.

Trade agreement talks are held with under the TPP program and with the EU to open up Japan’s economy to global competition.

Macroeconomic policies aim to stabilize the Japanese Government debt and to stop “deflation”.

According to Professor Hoshi, the Prime Minister Abe’s Revitalization Strategy has around 150 different action areas, and some of them are very good ideas, but others are terrible.

In particular Professor Hoshi criticizes that there are far too many action areas, and there is a lack of clear priorities and a lack of focus. It would be better to select fewer priority areas, and take strong effective action in these most important areas.

Professor Hoshi also sees a return to Government selection of “winning industries”. Unlike the time, when there was no internet, and when growth was a matter of copying the US or UK, Government today is in no better position than private industry to know which industries are which are likely to be the winners of the future.

One of the worst examples is the “Cool Japan” initiative: as soon as the Government supports anything, its not “cool” anymore, says Professor Hoshi.

Abenomics- Lack of strong Key Performance Indicators (KPI): only 19% of reform areas have any numerical KPI within 5 years

Growth strategies need clear numerical Key Performance Indicators (KPIs) – for many areas there are no KPIs at all, for others the KPIs are fuzzy and ill-defined (e.g. “Japan will become the most innovative country in the world”), or the KPI target date is so far in the future, that it is irrelevant for the current Prime Minister or the current Government, e.g. 2020.

Of 52 reform areas in the Government’s growth strategy program:

10 areas have no KPIs at all, i.e. the Government cannot measure if any progress is achieved at all in these areas

Only 10 of 52 areas (only 19%) have any numerical KPI within 5 years.

In many cases the KPIs are ill-defined and fuzzy: e.g. “Japan to become the most innovative country in the world”, or target dates in 2020, i.e. irrelevant and out of the responsibility of the current Government and the current Prime Minister

Special zones – risk to redistribute economic activity geographically within Japan with zero net effect.

Special zones where regulations and approval conditions are relaxed are ideas which have been floated for a long time in Japan. The disadvantage of “special deregulated zones” is that economic activity is just redistributed in Japan, moving from regulated zones to deregulated “special zones” with zero net effect on Japan’s economy, or even increasing the total cost of doing business in Japan.

Abenomics – Reheated pizza?

In conclusion of his talk, Professor Hoshi showed the following slide, which shows the vision of a transition from present Japan (left) to the Japan of the Future (right):

Professor Takeo Hoshi

The image of this slide is from Prime Minister Koizumi’s revitalization plan of 2001, i.e. 12 years ago. Professor Hoshi uses this slide to make the point that in his view not much has changed since 2001, that Prime Minister’s Abe’s revitalization plan is not very different from Prime Minister Koizumi’s revitalization plan 12 years ago, and he remains skeptical of Abenomics and its chances for success.

Abenomics success – Q & A

Q. What is the probability for Abenomics to succeed?

A. I was asked this question previously and from the top of my head I instinctively answered that Abenomics has about 10% probability to succeed. I got intrigued, and sat down to work through a decision tree of different policies, and the result was: Abenomics has 12% probability to succeed, and 88% probability of failure

Q. What do you think is the most likely scenario?

A. Something like what happened under Prime Minister Koizumi. About 1% economic growth, but not 2%-3%

Q. Management of Japanese companies?

A. Many major Japanese companies pile up too much cash, should invest more, and pay more to shareholders.

Lecture summary written by Gerhard Fasol, with revisions by Mr Masamoto Yashiro. All Rights Reserved.

Masamoto Yashiro: Japan leader and Chairman emeritus of Esso, Exxon, Citibank, Shinsei Bank, Board Director China Construction Bank

Masamoto Yashiro at brainstorming by President of Tokyo University

Masamoto Yashiro is a legend in Japan’s banking and energy industry. He built Shinsei Bank from the ashes of the bankrupt Long Term Credit Bank of Japan, and served in leadership positions (Chairman, CEO, Board Member) in Esso, Exxon, Citibank, Shinsei Bank, and the China Construction Bank.

Tonight a small group of about 60 people were invited to join Masamoto Yashiro and the President of The University of Tokyo, Professor Junichi Hamada, for an evening workshop and brainstorming event about globalization of Japanese corporations at The University of Tokyo. Participating were a selected group of The University of Tokyo graduates, faculty, and selected alumni from several elite Universities associated with The University of Tokyo, and currently working at major Japanese trading companies, Ministry of Finance, financial firms, global consulting firms and other global firms.

After The University of Tokyo President Junichi Hamada’s introductory words, we heard Masamoto Yashiro’s fantastic overview of how he thinks Japanese companies need to change and why, followed by Q&A, then by a brainstorming session in the format of changing groups of four on about 15 separate tables between the participants, and then followed by buffet and drinks reception.

Topic of the evening was the globalization issues of Japanese corporations, also discussed in our work about Japan’s Galapagos issues:

Masamoto Yashiro graduated from Kyoto University (Law Faculty) in 1954 and The University of Tokyo Graduate School in 1958, and entered Standard Vacuum Oil Company. In 1964 he became Director of Esso, and later Special Assistant to the Chairman of Standard Oil New Jersey, and in 1986 President of Esso Sekyu KK.

In 1989, Masamoto Yashiro moved to become Japan representative of Citibank NA, and Chairman of Citicorp Japan in 1997.

IN 1999, Masamoto Yashiro became CEO of New LTCB Partners CV, the company emerging from the bankruptcy proceedings of the Long Term Credit Bank of Japan, and was in charge of the revival of LTCB as Chairman and CEO, with investment from Ripplewood Investment Fund, creating today’s Shinsei Bank.

He resigned as CEO of Shinsei Bank in 2005, but returned as Chairman and CEO in 2008, from which he retired in 2010.

In 2004, he was appointed Director of the China Construction Bank.

Masamoto Yashiro (former Chairman of Shinsei Bank, Chairman of Citicorp Japan and President of Esso Japan, Director of China Construction Bank)

Japanese management – why is it not global? What should we do? asks Masamoto Yashiro

Note: this record was reviewed personally by Masamoto Yashiro, who made some corrections.

Japanese management – why is it not global? Outline:

Some people may argue that Japanese companies need not be global. Why?

We must accept that English is an essential tool for international communication.

Some impediments that Japanese companies face:

The traditional approach is not effective in developing future leaders.

The Japanese-style board structure is not appropriate to ensure sound corporate governance.

Management structure needs to be changed to suit a global business.

The current limited role of foreign nationals in the management and board structure

What should be the most important corporate objective?

Concluding remarks

Masamoto Yashiro (standing at the podium on the right hand side) presenting and President of Tokyo University Junichi Hamada (sitting on the left) listening

Summary of Masamoto Yashiro’s talk:

Some people may argue that Japanese companies need not be global. Why?

Some superficial discussions about “Japanese companies” contrast “permanent employment” and excellent pensions in Japanese companies with job-hopping and bad pensions in other countries, however, Masamoto Yashiro points out that during his time at Esso and later Exxon, most employees stayed 20-30 years at Exxon, and received excellent pensions, so “permanent longterm employment” or pension system has nothing to do with globalization, and Japanese leading companies are no different than leading companies in other countries in these respects. We have to search elsewhere for the causes of current problems most Japanese companies are facing.

Around 1990, about 20 years ago, Japan was extremely self-satisfied by the successful reconstruction after the war and economic growth and success, and Japan felt that Japan does not have anything to learn from others. This time is now over, Japan is in stagnation, and many Japanese companies are not globally competitive, and Japan and Japanese companies must change to become competitive again.

We must accept that English is an essential tool for international communication.

Masamoto Yashiro is convinced that Japanese companies must globalize, and must make English a business tool. He feels it is a great disadvantage that Japanese political and corporate leaders, when participating in international conference, such as Davos, mostly need to use interpreters, and this reduces their global impact and exchange of ideas dramatically.

Some impediments that Japanese companies face:

1. The traditional approach is not effective in developing future leaders.

The traditional approach in Japan is to rotate career employees every two years between totally different functions, in order to “develop well-rounded managers”. The result of this process are non-experts, which are not expert in anything.

As an example, during his leadership at Shinsei Bank, Masamoto Yashiro once requested a meeting with the IT Department leadership. To his great surprise 60 people turned up for the meeting (he had expected 2 or 3). He asked the Department Chief for particular information, and he could not understand the question and could not answer, same result one management layer lower. Only at the third layer from the top, Masamoto Yashiro could get his question answered – the top two management layers could not answer his questions about the work of the IT Department.

Quite generally there often far too many people at meetings at Japanese companies.

When at Exxon in the US as a relatively junior manager, Masamoto Yashiro, was asked about his opinion regarding the termination of a particular joint-venture relationship with a mid-size petroleum refining company in Japan known then as ゼネラル石油精製 who had financial trouble. Exxon had a 50% interest in this company and its relations goes back to very late 1950’s. In late 1985 at the Exxon Management Committee meeting in New York, all other managers favored to terminate the relationship with this joint venture partner in trouble in order to limit financial exposure, while Masamoto Yashiro argued that it was better to support the troubled partner and assist him with Exxon staff and expertise to return to profitability. To his great surprise the Chairman and his superiors at Exxon sided with his recommendation and changed their previous position following his advice. Generally he felt that in the USA his opinion as a Japanese manager was highly valued, because it provided a different view point.

In his experience in Japan the situation is totally opposite: Japanese senior management generally does not listen to junior employees, and particularly not to foreign nationals in the rare cases that there are any in Japanese companies. In fact, the most frequent question senior management at Japanese banks ask, is not for original ideas or creativity from junior staff, but instead: “What do other banks do?”

This deplorable Japanese situation even contrasts strongly with the situation in China, where Masamoto Yashiro was a Director of the China Construction Bank: in China leaders moved from Government agencies and Ministries to Banks, and to private industries and back.

Generally Masamoto Yashiro expressed the view, that the development of leaders is totally inadequate in Japan, and is better in China than in Japan.

In addition to the inadequate development of leaders in Japanese companies, the number of foreign nationals in management, Board and other leadership positions in Japanese companies is minute, there are no programs to attract and develop foreign nationals in leadership positions. On the contrary, when Shinsei Bank showed losses in the aftermath of the Lehman shock, Japan’s Financial Services Agencies ordered that Shinsei Bank must pay all foreign nationals on exactly the same pay levels as Japanese employees. Since foreign nationals typically have much higher schooling and other costs in Japan than Japanese staff, essentially all non-Japanese staff at Shinsei Bank left soon after.

Leaders can make a real difference.

How leaders are selected is of utmost importance.

At Exxon, senior management devote specially reserved time to identify suitable candidates for future leadership positions, “who can potentially be our CEO in the future”. The selected candidates are given special attention and special opportunities to train and develop their leadership abilities. Masamoto Yashiro has never heard about such special leadership development programs at Japanese companies.

2. The Japanese-style board structure is not appropriate to ensure sound corporate governance.

In Japan, Board Members are almost always managing employees of the company, so the question arises who’s interests they represent on the Board. Do they represent the interests of the institution (the company), the employees or the interests of the shareholders.

In Japan often the CEO of the company after his retirement remains as a Chairman for several years, keeps his office, secretary and company car, and creates large other expenses. Why? Probably because Japanese CEO pay is too low, so that the CEO does not wish to retire gracefully.

This is totally different in Western companies where retired CEOs leave the company and have no further role in the company in most cases. Masamoto Yashiro mentioned the retired Chairman of Exxon, who after his retirement naturally travelled by taxi. In Japanese it would be unthinkable according to Masamoto Yashiro that the retired Chairman of a major corporation would travel by ordinary taxi cab like ordinary people (Masamoto Yashiro did not mention subway or bus, or driving his own personal car….)

3. Management structure needs to be changed to suit a global business.

In non-Japanese companies in almost all cases have a thorough performance evaluation system. When performance is evaluated, the resulting distribution must be similar to a normal distribution, i.e. with considerable part of employees at the high end and substantial numbers at the low end of the performance curve. If this is not done, top performers cannot be sufficiently rewarded and will leave the company, while low performers would hold the whole company back.

In most Japanese companies on the other hand, if a thorough performance evaluation is done at all, in most cases a huge proportion of employees are just evaluated as average, satisfying performance, without clear distinctions between top and bottom performance.

Promotion and salary on the other hand in traditional Japanese companies is purely according to age, which leads to many problems, and causes under-performance of the whole company.

These problems are increased by the fact, that Japanese companies typically do not give the same evaluation or opportunities to non-Japanese nationals.

4. The current limited role of foreign nationals in management and board structure.

Even in the rare cases where foreign nationals are employed by Japanese companies in management or leadership positions e.g. in foreign subsidiaries, often junior Japanese employees which much lower rank and local knowledge do not respect and bypass non-Japanese management, and there is typically no fair evaluation system, evaluating Japanese and non-Japanese management according to the same standards of performance.

The change of this mindset (to keep non-Japanese out of management or leadership positions at Japanese corporations) is extremely important.

The change of mindset (to keep non-Japanese out of management or leadership positions at Japanese corporations) is not difficult at all and can be done quickly.

What should be the most important corporate objective?

When considering corporate governance it is important to develop a view on the objectives. When discussing the interest of shareholders, it is important to ask “which shareholders”? The interests of large shareholders who may own 10% or 20% of the corporation, or the interests of individual smaller shareholders? Other stake holders’ interests also need to be taken into account.

In general, Masamoto Yashiro expressed the view that both the institution’s (the company’s) and the shareholders interest are best served by stable long-term growth of the company. He mentioned as an example Exxon which showed triple-A rating and annual rate of growth of 15%-17% for over 100 years.

Concluding remarks.

Around 1990 Japan was self-satisfied with the economic success, and Japanese people thought that they have nothing to learn from anybody. This time is over now, and Japan and Japanese corporations much change to regain growth and to become competitive again.

Professor Junichi Hamada, President of The University of Tokyo, listening to Masamoto Yashiro’s talk

Japanese management – Q&A with Masamoto Yashiro (selected questions)

Q. You want Japanese companies to change. What are the good things you want Japanese companies to keep?

A. Loyalty. Consideration to stakeholders.

Q. Your work at Shinsei.

A. Communication was most important. When Masamoto Yashiro took over at Shinsei, the Bank has just gone through bankruptcy proceedings, so the moral was extremely low. Masamoto Yashiro had to reestablish optimism and moral. To do so, communication is most important. Masamoto Yashiro held weekly telephone conferences and every employee who wanted to could participate: from top management to cleaning staff/janitors. Everyone could come forward with his concerns.

Another fact was that there were so many traditions which made no sense. For example, female employees with University degrees would wear their own clothes, while female employees without University degrees would need to wear company uniform. There was an issue that lower paid staff had difficulty to afford appropriate clothing for bank work – so Masamoto Yashiro decided to award a clothing allowance to employees so that they could afford appropriate clothing.

Q. Many Japanese companies cannot hire young employees, because they cannot fire/discharge non-performing older employees.

A. Firing/discharge of non-performing employees can be done by paying adequate severance compensation. Considering that a non-performing employee who remains on the payroll for several years in addition to salary also creates a lot of secondary costs, it is typically cheaper to pay an appropriate severance package, and most people are happy to leave with an appropriate severance package, and often move to a more suitable position at a different company – this helps everyone. Of course some companies want to save money at all cost, and fire employees without adequate package and that can lead to problems.

Q. Having worked much of your career at global oil or energy companies, what to you think about Japanese oil companies?

A. Japanese oil companies are not really oil companies, because they do not invest enough upstream.

Q. Leadership?

A. Japanese companies must change. The mindset must change.

Q. University of Tokyo?

A. University of Tokyo at the moment I think is ranked on 30th or 40th position globally in most rankings, maybe top in Japan or in Asia, but that does not count, we need to look at the whole world, not just Japan or Asia. I think University of Tokyo should make the changes necessary be at least in the top ten globally. To get into the top ten globally, University of Tokyo needs to hire outstanding Professors where the best students from the whole world want to come and study. To get the best Researchers and Professors University of Tokyo has to pay what is necessary. Does not matter which language, English or Japanese or any other language. No outstanding student from other parts of the world wants to study Japanese first before studying at University of Tokyo. University of Tokyo should make the necessary changes so that the best students from top Universities globally also want to come to University of Tokyo.

Mr Masamoto Yashiro’s talk and Q&A were followed by a brainstorming session in groups among all participants of four about globalization, and global leadership development.

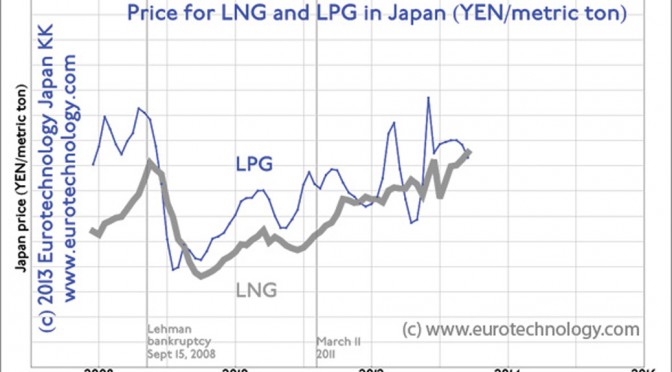

Was invited today to take part in a discussion meeting at one of the European Embassies about pricing of Gas (LNG) imports.

All the major Japanese buyers of LNG from the major electricity and gas companies came together with European partners to discuss issues of import Gas (LNG) pricing.

For detailed statistics of Japan’s gas (LNG, LPG) imports, and why Japan pays so much more than any other major country for LNG read our Report on Japan’s energy sector

Japan Galapagos Effect – how to capture global value for Japan. From the Journal of the American Chamber of Commerce in Japan (ACCJ), reproduced with permission.

Dr. Gerhard Fasol dissects the history behind Japan’s unique international market separation

Originally posted by ACCJ Journal on January 15, 2011 in “Chamber Events”

based on a talk given by Dr. Gerhard Fasol to the Members of the American Chamber of Commerce (ACCJ) on July 12, 2010, at the Westin Hotel, Tokyo.

(c) 2011 Copyright by The American Chamber of Commerce in Japan (ACCJ).

Reproduced with kind permission of ACCJ.

Dr. Gerhard Fasol, the founder and CEO of Eurotechnology Japan KK, spoke to ACCJ members about Japan’s “Galapagos Effect” at the Westin Hotel in Tokyo. The “Galapagos Effect,” for those unfamiliar with the term, is used to describe Japan’s unique culture of technology that has not expanded beyond Japan’s borders, in the same way that the Galapagos Islands exemplify unique evolutionary developments in nature.

Gerhard Fasol

Where Japan Leads

Investment is a prime reason why such developments as Internet-related mobile communications are so advanced in Japan. As Fasol pointed out, Japan has seven times the number of 3G base stations as the United Kingdom. Many of the related technical developments in mobile handsets that are only just coming onto the market outside Japan have been standard for many years in this country—Fasol gave high-quality camera phones as an example.

Quoting a Nokia spokesman, he claimed one reason for this leap was that Europe is conservative in regards to standards, which take a long time to develop and ratify in contrast to Japan. He amplified the Galapagos analogy by stating, “Japan is a Galapagos island, and doesn’t have to care about standards.”

Fasol also claimed that Japan is 10 to 15 years ahead of other nations in its use of electronic money. He contrasted Europe’s fragmented and overly bureaucratic nature with Japan’s, where large decisions—such as

i-Mode and Suica—can be made by a mere two or three people, which may come as a surprise to those who see Japan as a bureaucratic nightmare.

The reverse side of the Galapagos effect, however, is that Japanese phones designed for the home market fail to find buyers outside Japan. Electronic money is another area where Japanese technology seems destined to remain within the borders of Japan, despite the fact it is now quite common and accounts for a relatively large proportion of currency in circulation at about two percent. Fasol claimed that the U.S. and Europe are not yet ready for the mass introduction of such a payment system like Japan. In the long term, he believes, non-Japanese global giants will probably win out over the Japanese innovators.

Shedding Light on Genius

Another area where Japan has led innovations in the commercialization of technology is the revolution in lighting, which is poised to offer new environmentally-friendly illumination options. Based on the invention of the blue LED by Shuji Nakamura, the new lighting systems are also wallet-friendly in that they offer a 6,000-fold advantage in terms of price for the same amount of light over kerosene-powered lighting, still a staple in many parts of the world.

However, Nakamura was largely ignored by the Japanese business community; he is not even named on the website of the company that employed him (Nichia), and is now working at a university in California—Tokyo University claimed they wanted more “ordinary professors.” According to Fasol, the “Galapagos effect” means that there is no room or need for geniuses like Nakamura in Japan.

Economy

Up to 1995, Japan’s economy was growing, but is now static, a unique situation within the G8. Indeed, extrapolated from present trends, South Korea’s economy could overtake Japan’s in 2022.

Japan has a huge electronics sector, from giants to smaller specialist makers with a $600 million market about the same as the Netherlands. However, the growth is almost zero compared with that of 10 years ago. The net income of the top 20 companies of the sector is actually less than that of a single U.S. company, GE or of Korean rival, Samsung. This has a disadvantageous effect on pension funds, who are the major shareholders of these companies, but the governance of Japanese corporate affairs by shareholders is much less than, say, in the U.S. Still, Japan enjoys a very large national market (unlike the UK, for

example), which can help companies survive. On the other hand, this may have prevented companies from “going global” as their internal market has reached saturation. Fasol mentions rice cookers as an example of a

consumer durable that is not purchased frequently, and accordingly has a relatively small and finite market footprint. Even so, every major electrical manufacturer designs and produces a range of rice cookers, with a very low profit margin of well under one percent, which may be part of the legacy of the zaibatsu (the large pre-war conglomerates). This legacy means that most present-day conglomerates feel the need to do everything—for instance, there are three global makers of trains, but ten in Japan.

The Galapagos Study Group

Fasol then went on to describe the 26-person interdisciplinary Galapagos Study Group—of which he was the only non-Japanese member—which met monthly for a year and concentrated on the mobile phone industry.

The results of these meetings were summarized in three sets of recommendations to telecom carriers, electrical manufacturers, and content companies, with the second category receiving the recommendations that Fasol described as most radical.

He surprised his listeners by saying, “I think it would be best for Japan if in five years or so there were no more Hitachi, or Fujitsu, or Toshiba.” This, of course, was not meant as a direct attack on these specific companies, but as an attack on their conglomerate nature. Instead of the current state, he suggested a move towards smaller companies, focused on profitable businesses, would be preferable and would restart growth.

On the content side, Fasol claims that Japan is the only country in the world with the intellectual and creative resources to create characters that can stand up to Mickey Mouse and the Disney empire, but has not succeeded in creating global businesses based on Pikachu or Doraemon. Accordingly, the committee made a recommendation that platforms similar to Disney be created in order to create global businesses using such characters.

Gerhard Fasol

Coming to Japan from the Outside

On the subject of breaking into “the Galapagos market,” Fasol pointed out that good foreign companies can succeed in Japan if they know the market. As an example, he cites traffic lights, whose specifications in Japan are controlled by the police. Any company failing to recognize this kind of local quirk, no matter what its global standing, is doomed to failure when it comes to Japan. Examples of dramatic failures he cited were Nokia, Nasdaq, and Vodafone. To paraphrase the traditional real estate tag, Fasol claimed that the three biggest mistakes foreign companies coming to Japan make are “arrogance, arrogance and arrogance.” He claimed that this has nothing to do with Japan’s closed markets, quoting the iPhone’s success as an example.

He pointed out that there are other reasons for the failure of foreign entrants. Apart from the failure to listen to customers and understand the market, reasons include partnership with the wrong joint venture partners, and the management of Japanese ventures by managers who fail to understand the country.

However, the Japanese service lifestyle, allied with what he terms a “fashion society,” is a great opportunity for outsiders to break into the Galapagos market, and Fasol claimed that foreign companies can tap Japan’s creativity and use it to their advantage.

He also claimed that the relative isolation of Japan from global standards and practices in some cases actually enriches the global experience. But at the same time this also introduces life-threatening issues for Japan and this isolation must be addressed through two-way dialog from inside and outside of Japan.

(c) 2011 Copyright by The American Chamber of Commerce in Japan (ACCJ).

Reproduced with kind permission of ACCJ.

—–

Gerhard Fasol’s Stanford University lecture “New opportunities vs old mistakes – foreign companies in Japan’s high-tech markets”

(was transmitted by Stanford’s TV to 100s of Silicon Valley companies)